The era of New Space shows that space is no longer a distant story of the future. The rapidly growing space industry is emerging as a solution to global challenges such as the climate crisis and big data, while also increasingly influencing daily life. From the morning weather forecast to messages exchanged with friends, space technology is creating new value in every aspect of life.

But where does this value originate within the space industry’s value chain, and where does it lead? More importantly, what are the hidden opportunities within this value chain?

The Era of Transformation in the Space Industry

The aerospace sector is experiencing exponential growth driven by increasing investments from private companies and venture capital. The space economy is projected to expand from $630 billion in 2023 to an astounding $1.8 trillion by 2035, outpacing global GDP growth rates. The positive outlook for the space industry is reflected in the growing scale of investments by global venture capital firms, with 13 of the top 15 VC firms worldwide now actively investing in the sector.

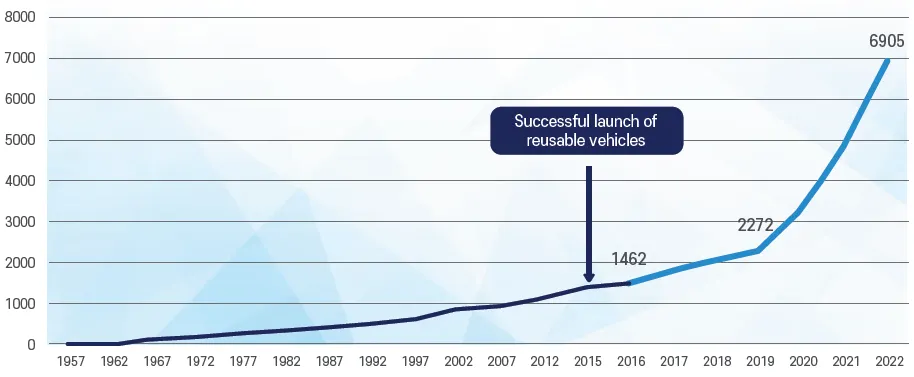

The space industry is entering a phase of advanced maturity and full-scale commercialization. One of the key accelerators of this transformation is the declining cost of launch vehicles, which has sparked innovations across the entire value chain. At the heart of this cost reduction lies the reuse of launch vehicles, which account for up to 80% of production expenses. Thanks to SpaceX’s pioneering advancements in reusable rockets, the cost curve for satellites has plummeted dramatically. This reduction has ushered in the era of satellite constellations.

Moreover, as upstream startups such as SpaceX reach maturity, momentum is shifting to the midstream and downstream sectors. The downstream industry, in particular, holds enormous potential, generating an additional $9.8 billion in value for every 1% increase in its user base. This growth signifies the emergence of entirely new markets that previously did not exist.

SpaceX’s launch vehicle at Kennedy Space Center, USA.

A New Satellite Paradigm: Low-Earth Orbit Satellites

The growth of the space industry is evident in the soaring number of satellites being launched. From 2019 to 2023, the number of satellites launched annually has grown at an average rate of over 50%. As of May 2024, there are approximately 9,900 satellites orbiting Earth, with a staggering 84% of them classified as low-Earth orbit satellites (LEO).

The mainstream adoption of small LEO satellites is a relatively recent phenomenon. In the 1990s, small satellites accounted for roughly 34% of all launches. By 2020, they made up 94% of all deployed satellites. Alongside this trend, numerous small and medium-sized satellite manufacturers have emerged, developing satellites not only for traditional Earth Observation (EO) purposes but also for a variety of other observation and communication needs.

This surge in small satellites is expected to drive further reductions in the cost of satellite data, which is projected to decrease by over 10% by 2035. This trend underscores the growing accessibility and integration of space-based data into everyday applications.

Source: Statista, restructured by Gravity Ventures.

Satellite Data: The Key to Unlocking Innovation

With the growing number of satellites, the satellite application industry—particularly in space-based internet—is experiencing a surge in demand. Currently, global internet penetration stands at only 59.5%, leaving nearly half of the Earth underserved due to low population density, economic unfeasibility, and challenging environments such as polar regions. Faced with these inherent limitations of terrestrial internet, space-based internet has emerged as a complementary solution, significantly reducing CAPEX (capital expenditures) and enabling a move toward hyperconnectivity.

The space internet market, pioneered by Starlink with low-Earth orbit (LEO) satellites, has already demonstrated its commercial viability, achieving profitability last year. The race to capture the remaining underserved areas has become the driving force of the current satellite industry.

The era of hyperconnectivity is now approaching, where satellites, aircraft, and terrestrial networks converge into a unified ecosystem. This marks the dawn of the 6G communication era, bringing about a future of ultrafast and seamless connectivity.

* CAPEX(Capital expenditures)

Also referred to as capital expenditures (CAPEX), this term denotes costs incurred during the investment process aimed at generating future profits or acquiring long-term value.

Source: Statista, restructured by Gravity Ventures.

Developing Space Optical Communication: A New Paradigm

For satellites to achieve meaningful innovation, advancements in the communication industry are essential to overcome the bottleneck in the value chain. Since the 1950s, the space industry has made remarkable progress. However, communication technology in space has remained reliant on frequency-based wireless methods, much like in the 1950s. Despite significant innovations in satellites, limitations in speed and capacity have resulted in vast amounts of data being discarded in space.

Today, space optical communication has emerged as a superior alternative, offering unparalleled performance in speed, capacity, and reliability compared to wireless communication. This shift is akin to how optical fibers revolutionized high-speed internet on Earth.

As space optical communication garners more attention, the industry surrounding optical communication equipment is also gaining prominence. Since lasers are used to transmit data across free space, more precise targeting and correction between ground stations and satellites are required. The future focus will be on overcoming the limitations of laser communication through technologies like adaptive optics and precision tracking, thereby further bridging the gap between space and Earth. It is crucial to support startups addressing this bottleneck between the midstream and downstream sectors of the value chain.

Example of satellite-based space optical communication.

Expectations for the Space Industry and Jeju’s Role

Global VC powerhouses that have historically led paradigm shifts are now rapidly increasing investments in the space industry, identifying it as the next-generation growth engine. Notable top-tier venture capital firms such as Sequoia Capital and Andreessen Horowitz have been at the forefront of this movement. Their investment portfolios span the entire value chain, and between 2015 and 2022, the number of transactions in the space sector has at least doubled, while investment volume has grown more than fivefold.

Moreover, the share of investments in profitable companies rose dramatically—from 56% in 2015 to 95% in 2022—indicating the industry’s maturity and the onset of full-scale commercialization.

The space industry is poised for significant growth. I hope Jeju will play a pivotal role as a strategic hub for the space industry, not only in Korea but also globally. As an investor, I am committed to supporting the full lifecycle of Jeju-based space startups, from discovery and cultivation to investment and global expansion.